Rent Growth Remains the Missing Piece in the Multifamily Recovery

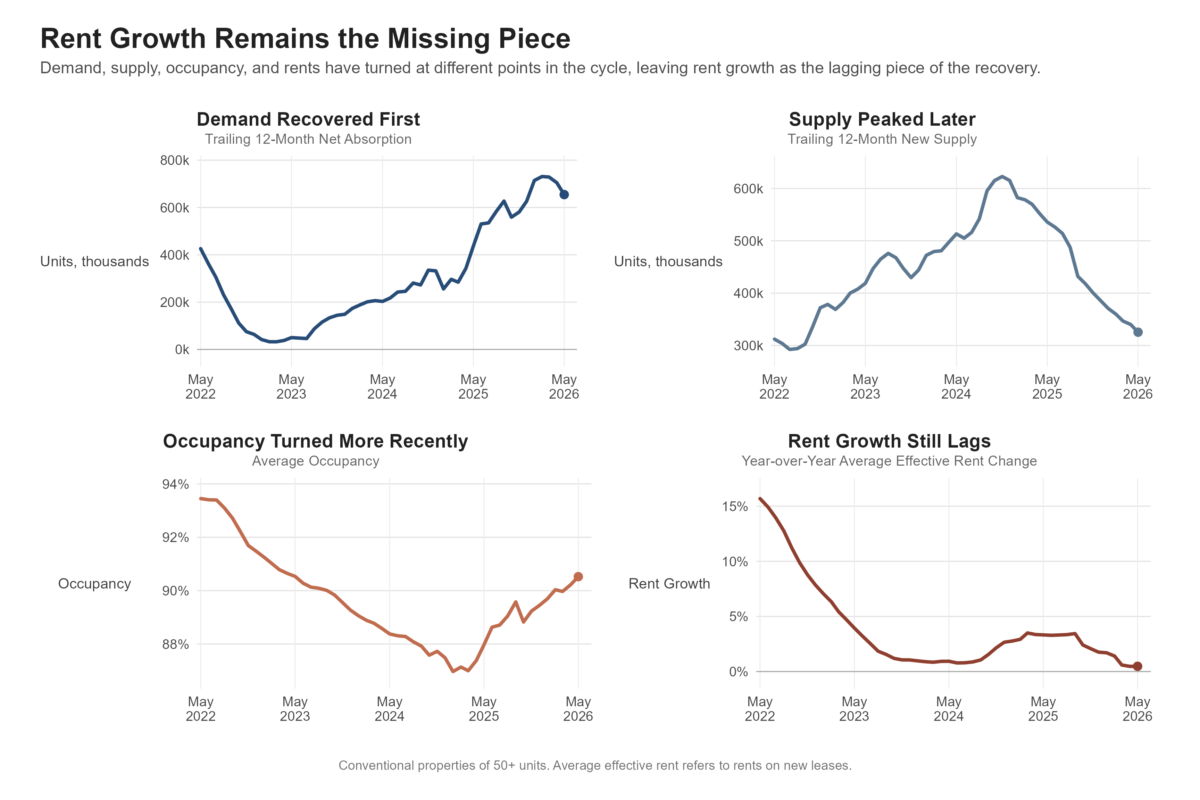

The national multifamily sector entered the early phase of recovery last year. New supply peaked in 2024, apartment demand finished 2025 on a three-year uptrend, and average occupancy began to recover. Coming into 2026, average occupancy still needed further improvement, the lease concession environment was a challenge, and rent growth had yet to rebound.

With supply-demand fundamentals healthier than at any point since 2021, and occupancy slowly but steadily on the mend, rent growth remains the next piece of the recovery puzzle. One month of data should not be overstated, but May did provide an encouraging sign.

Methodology note: All figures refer to conventional properties with at least 50 units. Average effective rent refers to rents on new leases.

View the full monthly Markets Stats PDF

Affordability and Concessions Continue to Limit Rent Growth

Structural headwinds continue to limit rent growth despite improving multifamily fundamentals. The labor market has remained fairly resilient, though pockets of instability have emerged. Recent reacceleration has again pushed inflation ahead of wage growth. Residents have also largely been left to absorb the rent gains of 2021 and 2022 in most markets.

Occupancy is another constraint. Despite improving by about 260 basis points over the last 12 months, national average occupancy finished May at just under 91%. For properties that were already stabilized a year ago, average occupancy ended May at 93% – flat over the last 12 months. Both occupancy metrics remain below typical levels, limiting operators’ pricing power.

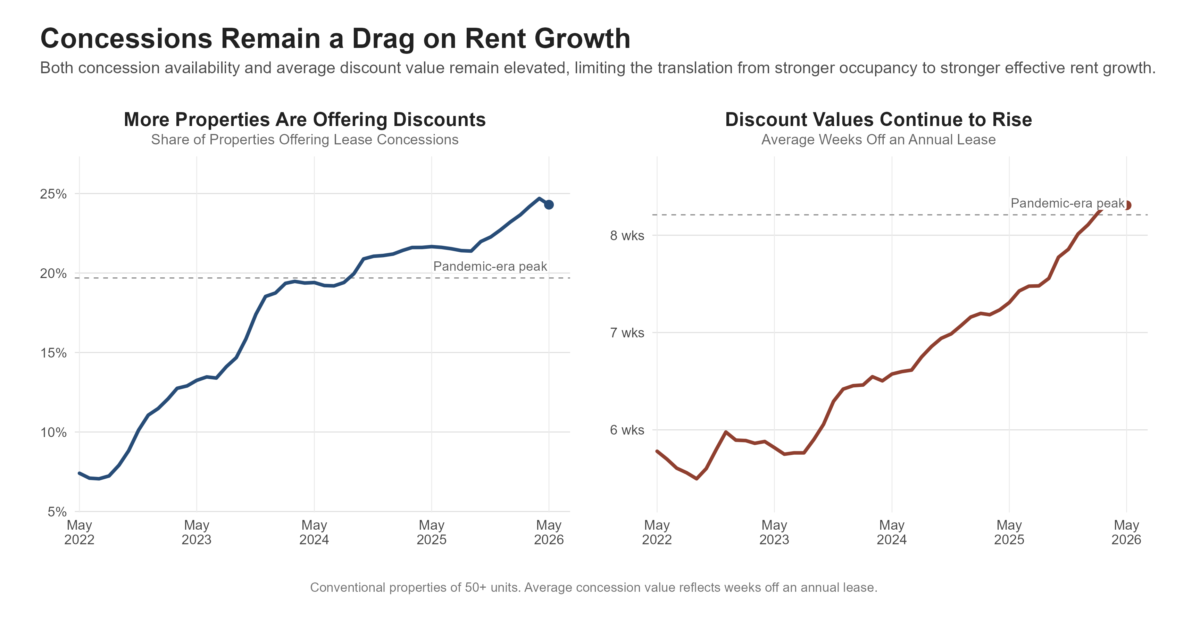

Lease concessions have also weighed on effective rent growth. Both concession availability and average concession value continue to rise. By the end of May, 24% of conventional properties nationally were offering a lease concession with the average concession equal to about 4.3 weeks off an annual lease.

Both concession metrics now exceed their pandemic-era peaks, particularly availability. The national figures also mask significant market-level variation. For markets that have been at the forefront of the supply wave, concessions are playing an even more prominent role. For example, in Austin 55% of conventional properties ended May offering a discount for new residents with an average value of six weeks off an annual lease.

May Provided Encouragement, but the Rent Growth Bar Remains Low

National average effective rent growth has failed to build momentum. Average effective rent rose 2.7% in 2024, then only 1.8% in 2025. Notably, last year’s annual gain had already been achieved by the end of May; rents were essentially flat for the rest of the year.

Monthly data provides useful context for the recent movement. National average effective rent rose 0.4% in May, the largest monthly gain since May 2025. In recent years, monthly rent change has remained within about 10 basis points of the May value in both June and July before beginning its seasonal cooling in August.

Year-to-date national effective rent growth stood at only 0.5% at the end of May. The May improvement was welcome given recent performance, but 2026 annual rent growth is unlikely to match the 2025 total and may struggle to cross even the 1% threshold.

Given rent performance so far this year, the more relevant question may not be whether 2026 can rebound to outpace 2025, but how much of the second-quarter gain may be given back in the fourth quarter.

Rent Growth Diverges by Price Class and Market

Rent performance softened across all price classes on a year-over-year basis. However, that softening has produced very different outcomes across price classes, reflecting clear differences in market conditions. Last month’s newsletter covered price class performance in detail.

At the top of the market, robust apartment demand has allowed lease concessions to begin easing. That early-stage drawdown has helped cushion the moderation in rent gains.

Class A average effective rent rose 2.7% over the last 12 months. That was below the 3.8% gain from the previous period but still led all price tiers over the last year. For Class B, rent growth slowed to just a 1.3% gain for the last 12 months.

Workforce housing has been the clearer drag on national rent growth. Lease concessions have become an increasingly important tool for driving leasing activity and they have taken a particular toll on effective rent performance.

Planning on attending or exhibiting at Apartmentalize? Come see us in Booth 1900 to talk about data and how we can help your business!

A 0.3% decline over the last year for Class C followed a 2.7% gain in the prior period. For Class D, a 1.8% gain from June 2024 through May of 2025 was followed by a 2.6% slide over the last 12 months.

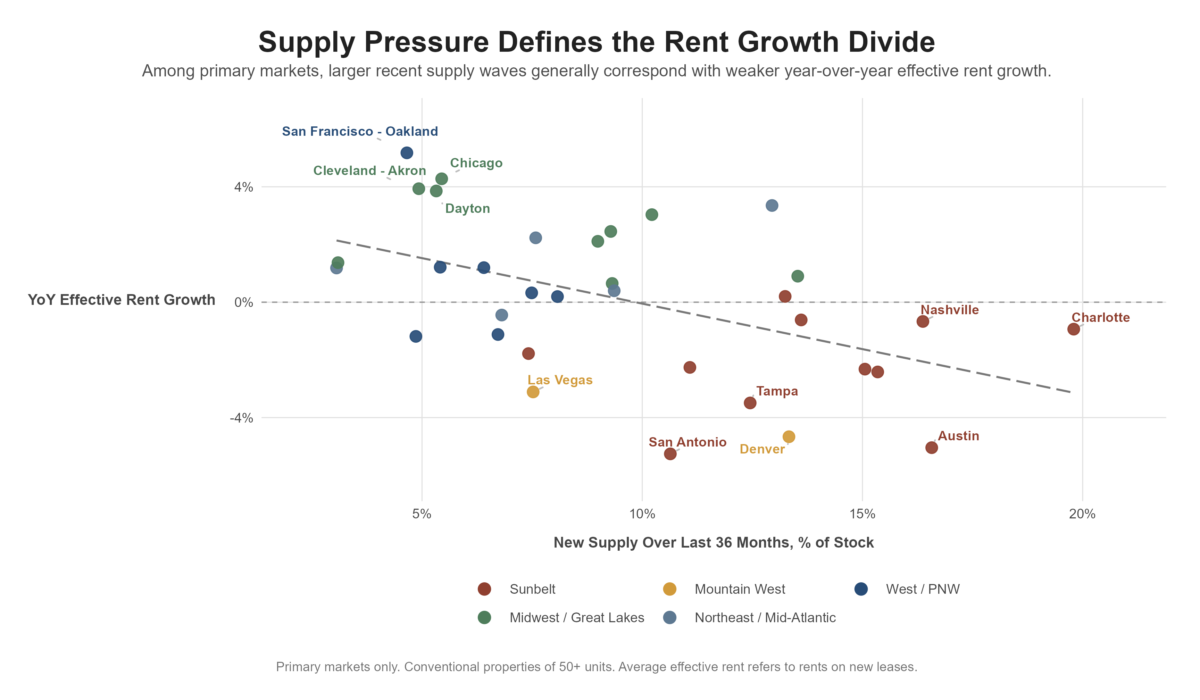

Regional rent performance has also diverged sharply. Much of the difference reflects recent supply pressure. Among the bottom 30 markets nationally for year-over-year average effective rent change, 29 were in either the Sunbelt or Mountain West.

Among primary markets, San Antonio, Austin, Denver, Tampa, and Las Vegas have recorded the largest recent declines. Each saw average effective rent decrease by 3% or more over the last 12 months.

At the other end of the spectrum, many of the largest gains have come from tertiary and micro markets. Among larger markets, the Great Lakes and Midwest regions are well represented. Markets such as Chicago, Cleveland – Akron, Dayton, Pittsburgh, and Minneapolis – St. Paul each added 3% or more to average effective rent over the last year. San Francisco–Oakland led primary markets with a 5% jump.

Takeaways

There is still plenty of reason for optimism in the big picture for multifamily. After peaking in 2024, new supply should remain more manageable through at least next year. Apartment demand has continued to post healthy results, though still with heavy reliance on lease concessions.

The improved balance between new supply and net absorption has allowed average occupancy to begin climbing out of a three-year hole. However, tightening fundamentals have not yet translated into stronger rent performance – and likely will not until next year. That may be little consolation to operators still facing elevated operating costs and intense competition for residents, but the broader multifamily recovery still needs more time to fully unfold.

Disclaimer: All content and information within this article is for informational purposes only. ALN Apartment Data makes no representation as to the accuracy or completeness of any information in this or any other article posted on this site or found by following any link on this site. The owner will not be held liable for any losses, injuries, or damages from the display or use of this information. All content and information in this article may be shared provided a link to the article or website is included in the shared content.